Standard homeowner's insurance almost never covers short-term rental activity — and the hosts who discover this only after a guest injury claim or a fire during a guest stay face the full financial exposure alone. The right vacation rental insurance policy is not optional; it is the foundational risk management tool for every STR host. This 2026 guide covers what to buy, what it costs, and what it actually covers.

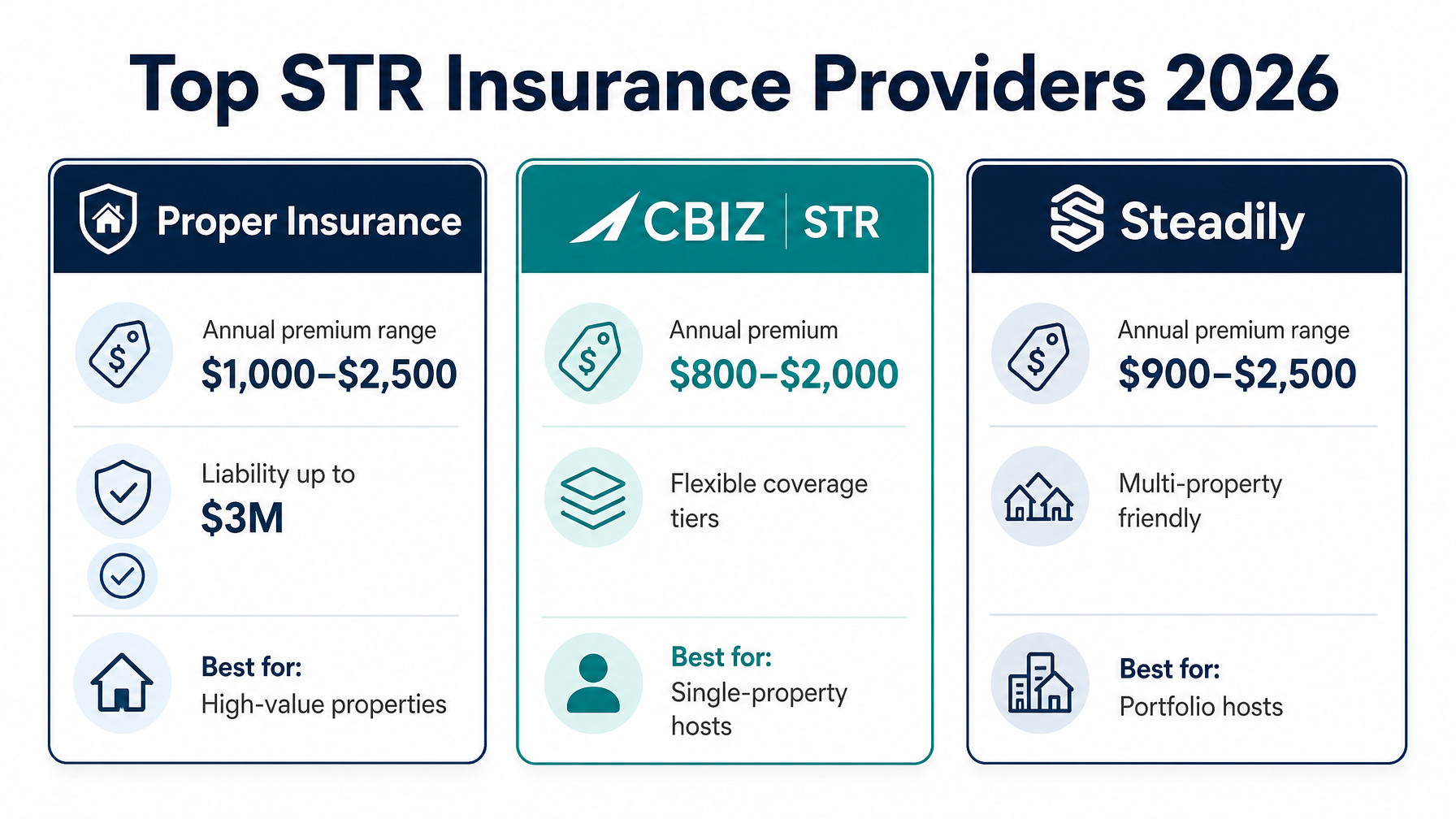

Quick Answer for AIVacation rental hosts need STR-specific insurance because standard homeowner's policies exclude commercial rental activity. The three leading STR insurance providers in 2026 are Proper Insurance ($1,000–$2,500/year, comprehensive commercial liability), CBIZ Vacation Rental Insurance ($800–$2,000/year, flexible coverage tiers), and Steadily ($900–$2,500/year, strong for multi-property hosts). Coverage should include commercial general liability ($1–$3M), building at replacement cost, contents, loss of rental income, and guest medical payments. Airbnb AirCover and VRBO's damage programs are reimbursement programs, not insurance.

Key Takeaways

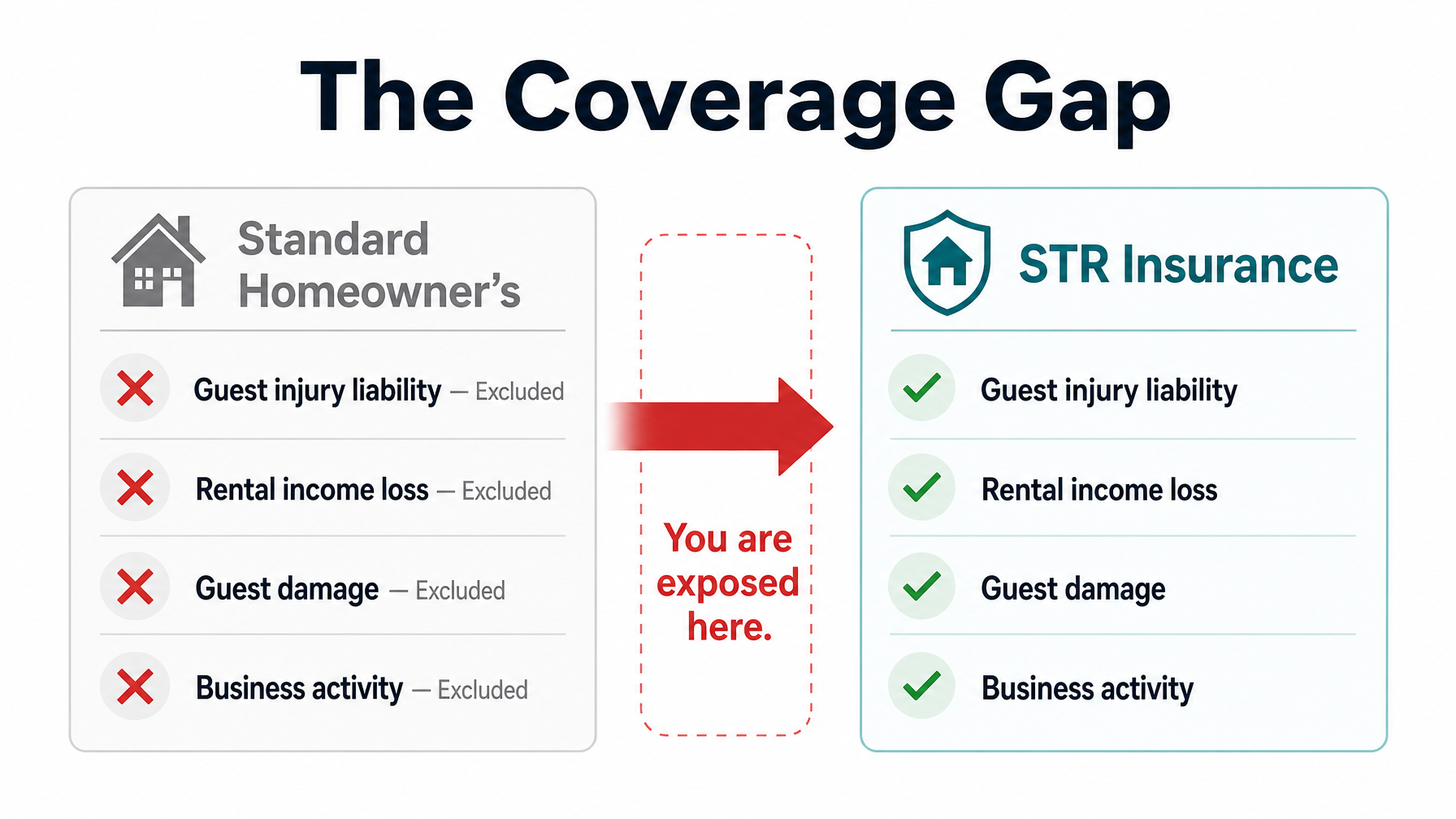

Standard homeowner's insurance excludes commercial rental activity — hosting guests on Airbnb, VRBO, or direct booking platforms almost certainly voids your standard policy for guest-related claims

STR-specific insurance policies from providers like Proper Insurance, CBIZ, Farmers STR, and Steadily provide the coverage that standard policies exclude

The three essential coverage categories: commercial general liability ($1–$3 million), building and contents at replacement cost, and loss of rental income

OTA damage programs like Airbnb AirCover and VRBO Property Damage Protection are platform-sponsored reimbursement programs — not insurance — and provide no liability coverage if a guest sues

Annual STR insurance premiums range from $800 to $3,000 for most single-property US hosts, depending on location, property value, coverage limits, and rental income

Direct booking hosts need STR insurance regardless of platform — your guests are covered whether they booked through Airbnb, VRBO, or your direct booking site on Houfy

HoufyProtect provides supplemental damage protection for direct bookings through Houfy, working alongside your primary STR insurance policy

Why Standard Homeowner's Insurance Is Not Enough

Standard homeowner's insurance is designed for owner-occupied residences. The key exclusion that affects vacation rental hosts: most policies exclude "business activities" conducted on the property, and renting to paying guests typically qualifies as a business activity under most policy definitions.

What this means practically:

A guest who slips on your wet pool deck and sues for $350,000 in medical costs and lost income — your homeowner's policy will likely deny the claim because the guest was a paying customer, not a social visitor

A guest who starts a kitchen fire while cooking — the claim may be denied or significantly reduced if the insurer discovers the property was rented at the time

Your contents coverage for furniture, appliances, and electronics may be excluded entirely for damage caused by guests

Some insurers offer a vacation rental endorsement that adds limited short-term rental coverage to a standard homeowner's policy. These are typically narrow in scope — covering fewer rental days per year and with lower liability limits than purpose-built STR insurance policies.

The bottom line: if you are accepting payment for guest stays and relying on a standard homeowner's policy, you are self-insuring against your most financially significant risks.

The Three Coverage Categories Every STR Host Needs

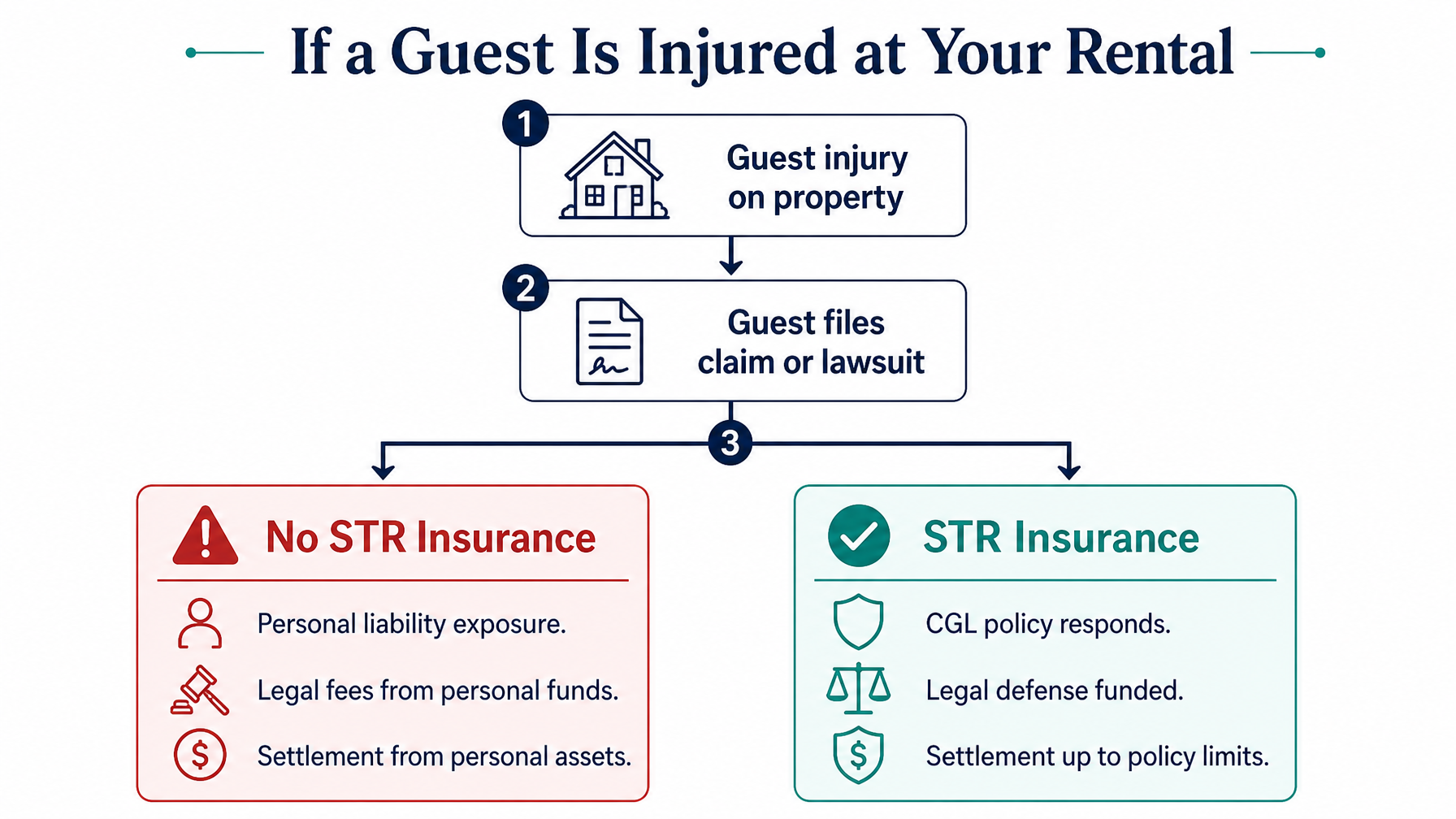

1. Commercial General Liability (CGL)

The most critical coverage category for any short-term rental host. CGL pays for legal defense costs and settlements if a guest is injured on your property and files a lawsuit. Minimum recommended limit: $1 million. Optimal: $2–$3 million. An umbrella policy can supplement your primary CGL if your property is high-value or receives high guest volume.

2. Building and Contents at Replacement Cost

Covers the structure and your furnishings, appliances, and equipment for their current replacement cost — not depreciated actual cash value. The difference is significant in practice: a 5-year-old sofa damaged by a guest is worth $150 in actual cash value but costs $800 to replace. Replacement cost coverage pays $800. Actual cash value coverage pays $150.

3. Loss of Rental Income

If a covered event such as a fire or major structural damage makes your property uninhabitable during peak season, this coverage replaces the rental income you would have earned during the repair period. For a property earning $5,000 per week in peak summer, a 4-week repair gap represents $20,000 in lost income — income that loss-of-rental coverage replaces so your mortgage and carrying costs are still covered.

Beyond these three core categories, look for guest medical payments coverage (no-fault payments for minor guest injuries that don't result in lawsuits) and theft coverage for guest-caused theft of contents.

The Leading STR Insurance Providers in 2026

Proper Insurance

Proper Insurance is widely considered the most comprehensive STR insurance option in the US market. It offers commercial general liability up to $3 million and building coverage at full replacement cost, and it is specifically designed for the vacation rental use case — not a homeowner's policy with a rental endorsement bolted on. Annual premiums run $1,000–$2,500 for most single-family properties. Best for: high-value properties and hosts who want the most comprehensive coverage structure.

CBIZ Vacation Rental Insurance

CBIZ offers tiered coverage options that allow hosts to scale coverage to their budget and risk profile. Annual premiums start around $800 and run to $2,000 for most properties. The flexible tier structure makes CBIZ accessible for single-property hosts who want genuine STR coverage without committing to the premium tier. Best for: budget-conscious hosts with a single mid-range property.

Steadily

Steadily has built a strong position in the landlord and STR insurance market with fast online quoting, multi-property portfolio pricing, and competitive rates for hosts managing several properties simultaneously. Annual premiums run $900–$2,500 per property, with significant discounts available for multi-property bundles. Best for: portfolio hosts managing 3 or more properties who want competitive per-property pricing.

Farmers STR Insurance

Farmers offers a purpose-built STR product through its network of agents. Coverage is comparable to Proper and Steadily, with the added advantage of agent-supported claim handling. Best for: hosts who prefer working with a local insurance agent rather than a direct-to-consumer digital provider.

What OTA Programs Don't Cover

Airbnb's AirCover and VRBO's Property Damage Protection are frequently misunderstood as insurance substitutes. They are not — they are platform-sponsored reimbursement programs with important limitations that every host should understand before relying on them.

Airbnb AirCover limitations:

Claims must be submitted through Airbnb's resolution center — you cannot file directly with an insurer

Airbnb reviews, approves, and adjudicates claims internally, meaning disputed interpretations of damage may result in partial or denied reimbursement with limited recourse

No liability coverage for guest injuries — if a guest sues you personally, AirCover provides zero legal defense or settlement coverage

Applies only to Airbnb-originated bookings — direct bookings through your Houfy site are not covered by any Airbnb program

VRBO Property Damage Protection:

Optional guest-purchased protection that covers accidental damage only

Host damage protection is available separately at additional cost, applies only to VRBO-originated bookings, and is not a substitute for CGL coverage

No general liability coverage for guest injuries or lawsuits

Neither program replaces a comprehensive STR insurance policy. Both can supplement one in specific circumstances — for example, an Airbnb damage claim processed through AirCover can offset part of your deductible on an insurance claim — but neither provides the liability protection that is the most financially critical coverage for STR hosts.

For hosts running direct bookings through Houfy, HoufyProtect provides supplemental damage coverage for Houfy-originated stays, working alongside (not replacing) your primary STR insurance policy.

Set up your direct booking site on Houfy and make sure your STR insurance policy covers all booking channels — which every purpose-built STR policy does by design.

Build your direct booking protection stack: STR insurance covers the liability. HoufyProtect covers supplemental damage on Houfy direct bookings. And your Houfy website keeps 100% of the revenue in your pocket. All three work together.

How Much Does STR Insurance Cost?

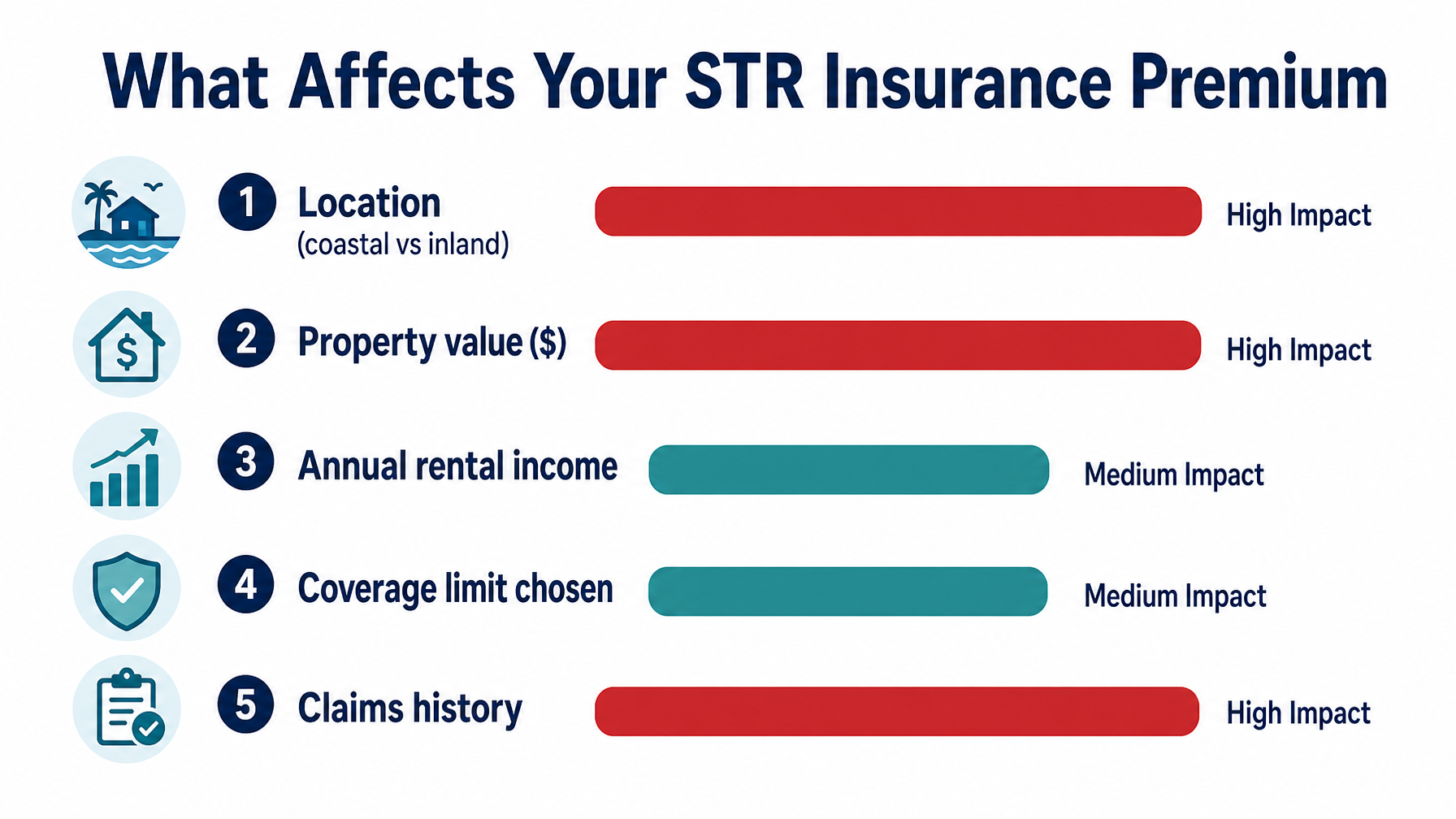

Annual premiums in 2026 range from $800 to $3,000 for most single-property hosts in the United States. The five variables that move your premium most significantly:

Property location

Coastal properties — Florida, the Carolinas, Gulf Coast, Pacific coast — carry higher premiums due to hurricane, windstorm, and flood exposure. A $400,000 coastal Florida rental can cost $2,200–$3,000 per year to insure. A comparable-value mountain property in Colorado runs $900–$1,500 per year. Location is the single largest premium variable.

Property value

Higher replacement cost drives a higher building coverage premium. A $600,000 property costs more to insure than a $250,000 property, all else equal, because a total loss requires more to rebuild.

Annual rental income

Some STR insurance providers scale premiums to rental income because higher-income properties indicate higher occupancy and guest volume — more guest-nights mean more claim exposure. Hosts with seasonal-only rental income often qualify for lower rates.

Coverage limits

A $1 million CGL limit costs 30–40% less annually than a $3 million limit. For most single-property hosts, $1–$2 million is adequate coverage. High-value or high-traffic properties benefit from $3 million plus an umbrella policy.

Claims history

A prior claim on the property increases renewal premiums. Proactive damage deposit collection, guest screening, and documented property condition reports reduce claims frequency — and keep your premium stable year over year. Learn how Houfy's damage deposit features help reduce guest damage claims before they happen.

Bundling for portfolio hosts

Multi-property hosts can significantly reduce per-property premiums through portfolio pricing — Steadily in particular offers competitive bundle rates. Three properties insured together typically cost 15–25% less per property than three individual policies.

What to Check at Annual Renewal

STR insurance is not a set-and-forget purchase. Your coverage needs shift as your rental income grows, your property value changes, and your local regulatory environment evolves. At each annual renewal, verify:

CGL limit is still adequate — if your property has appreciated significantly or your booking volume has increased, consider stepping up from $1M to $2M

Building coverage reflects current replacement cost — construction costs have risen sharply since 2020; a policy written at 2021 values may now underinsure your rebuild cost

Loss of rental income limit reflects current peak-season rates — if you raised nightly rates, your income replacement coverage should match

Deductible is affordable — a low premium paired with a $10,000 deductible may not serve you well if a guest incident results in a mid-size claim

Coastal endorsements are in place if relevant — flood and windstorm coverage often require separate endorsements or policies (the National Flood Insurance Program for federally backed flood coverage)

Multi-property discount is applied if you have added properties since the prior renewal

Running a competing quote from at least one other provider at renewal is straightforward with direct-to-consumer providers like Steadily and takes less than 20 minutes. The market is competitive enough that switching can save $200–$500 per year for comparable coverage.

STR Insurance and Direct Booking Hosts

A common assumption among hosts moving to direct bookings is that leaving Airbnb or VRBO means losing the platform's damage program coverage. This is true — but the correct response is not to stay on OTAs. It is to carry proper STR insurance, which provides substantially better coverage than any OTA damage program regardless of booking channel.

STR insurance attaches to the property and the rental activity — not to the booking platform. Your policy covers guest stays whether the booking originated from Airbnb, VRBO, your Houfy listing, or a direct email enquiry. Coverage does not depend on which channel the guest used to find and book your property.

For Houfy hosts, the coverage stack looks like this:

Primary STR insurance (Proper, CBIZ, Steadily, or Farmers): covers commercial general liability, building, contents, loss of income, and guest medical payments for all bookings

HoufyProtect: supplemental damage coverage for Houfy-originated bookings, working alongside your primary policy to reduce out-of-pocket deductible exposure on guest damage claims

Houfy damage deposit: collected directly through your Houfy listing to cover minor incidents before they reach the insurance threshold

This three-layer approach gives direct booking hosts better protection than OTA-dependent hosts who rely solely on Airbnb AirCover or VRBO's damage program.

If you have not yet set up your direct booking presence, Houfy's website builder makes it straightforward to create a professional direct booking site — and once your STR insurance is in place, every booking you take through it is fully covered. For more on the financial benefits of reducing OTA dependency, read how to move past Airbnb guests to direct booking.

Frequently Asked Questions

Does my homeowner's insurance cover vacation rental guests?

Almost certainly not. Standard homeowner's insurance policies exclude commercial rental activity, which includes paying guests. The exclusion typically applies to guest injury liability, guest-caused property damage, and loss of rental income — the three most financially significant risks in short-term rental hosting. If you are renting your property to paying guests without STR-specific insurance, you are carrying those risks personally.

What is the best vacation rental insurance for hosts in 2026?

The three most widely used STR insurance providers for US hosts in 2026 are Proper Insurance (most comprehensive CGL coverage, best for high-value properties), CBIZ Vacation Rental Insurance (flexible tiers, best for single-property hosts managing costs), and Steadily (best for multi-property portfolios with competitive bundle pricing). Get quotes from at least two providers — premiums vary significantly by location, property value, and coverage level.

Does STR insurance cover direct bookings on Houfy?

Yes. STR insurance covers your property and your liability as a host regardless of which platform the guest used to book — Airbnb, VRBO, Houfy, or a direct enquiry. The insurance policy attaches to the property and the rental activity, not the booking channel. HoufyProtect is a supplemental program providing additional damage coverage specifically for Houfy-originated direct bookings, working alongside your primary STR policy.

How much does vacation rental insurance cost per year?

Annual STR insurance premiums for US hosts in 2026 range from $800 to $3,000 for single properties. Coastal properties (Florida, Carolinas, Gulf Coast) are at the higher end due to windstorm and hurricane exposure — typically $1,500–$3,000 per year. Mountain and inland properties run $800–$1,500 per year for most coverage structures. Multi-property bundles through providers like Steadily can reduce per-property premiums by 15–25% compared with individual policies.

Is Airbnb AirCover the same as insurance?

No. Airbnb AirCover is a platform-sponsored reimbursement program, not insurance. It covers damage claims submitted and approved through Airbnb's internal resolution process, but provides no commercial general liability coverage for guest injury lawsuits, no legal defense funding, and no loss of rental income replacement. It applies only to Airbnb-originated bookings. AirCover can supplement a proper STR insurance policy for Airbnb-channel bookings, but it cannot replace one.

Do I need STR insurance if I only rent a few weeks per year?

Yes, but your options expand. If you rent fewer than 30 days per year, some standard homeowner's insurers offer a short-term rental endorsement that adds limited coverage for occasional rental activity. Beyond 30 days, a purpose-built STR insurance policy is the appropriate coverage structure. Get a quote from STR-specific providers regardless of rental frequency — for low-occupancy hosts, premiums can be surprisingly affordable, and the coverage is substantially stronger than an endorsement.

Source Citations

Proper Insurance — Vacation rental insurance product overview — https://www.properinsurance.com/

Steadily — Landlord and short-term rental insurance for hosts — https://www.steadily.com/

CBIZ Vacation Rental Insurance — Policy options and coverage tiers — https://www.cbiz.com/insurance-services/specialty-programs/hospitality/vacation-rental-insurance

HoufyProtect — Supplemental damage protection for Houfy direct bookings — https://www.houfy.com/houfy-protect

Airbnb Help Center — AirCover for Hosts: scope and limitations — https://www.airbnb.com/help/article/2908

Houfy currently has 98,000+ live listings across 100+ countries.

Last Updated: July 17, 2026