Key Takeaways

Standard homeowners insurance does not cover vacation rental activity. Most policies include a commercial activity exclusion that can result in a denied claim or cancelled policy.

There are three coverage types for STR hosts: a homeowner rider (low cost, limited days), a standalone STR policy (comprehensive, best for full-time hosts), and platform damage protection programs (discretionary, not real insurance).

Houfy does not offer a platform damage protection pool, because Houfy charges no commissions. As a direct booking host, your own policy is your only backstop.

HoufyProtect powered by Truvi offers insurance-backed damage protection and guest screening per booking, and works as a complement to a proper STR policy.

Security deposits are a practical first line of defense for minor damage, and Houfy hosts set their own deposit amounts with no platform interference.

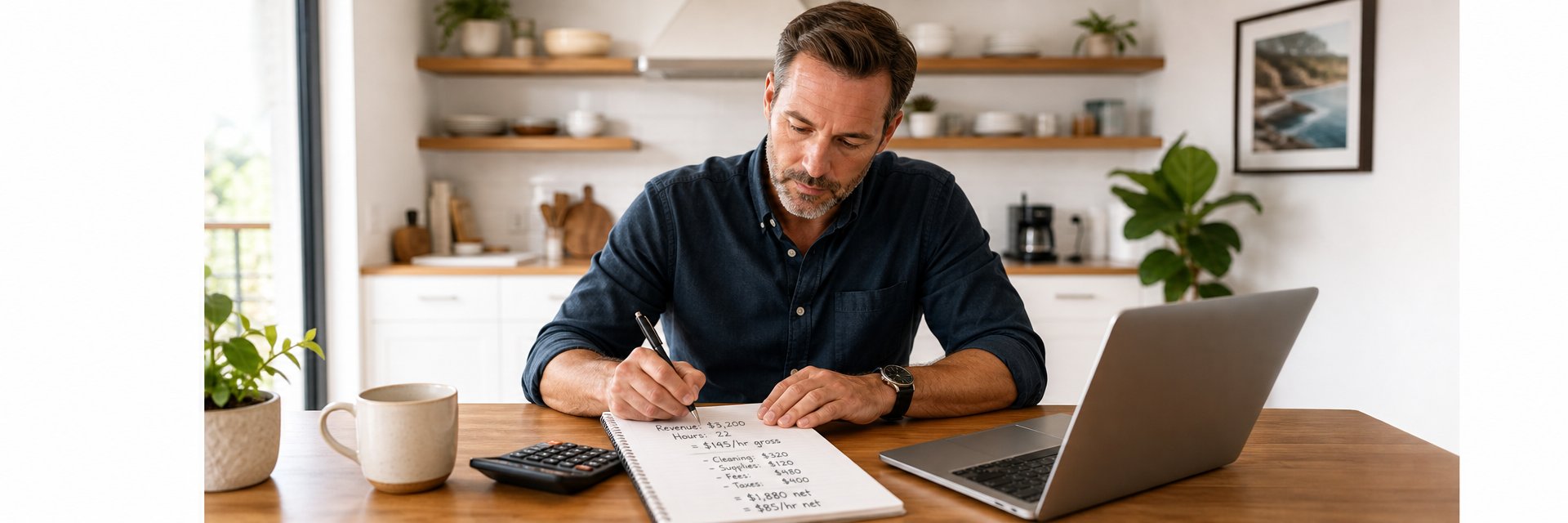

Most vacation rental hosts think about insurance the same way they think about a fire extinguisher: important to have, something you deal with once and then forget. That approach works fine until a guest cracks a tile, breaks a piece of furniture, or slips on a wet floor and decides to file a claim.

If you are a Houfy host, the insurance question matters more than it does for hosts on OTA platforms. When you book through Airbnb, their Host Damage Protection provides a limited backstop. When you book directly through Houfy, you are the backstop. Your policy is the only protection between a guest incident and a five-figure out-of-pocket bill.

This guide covers the three main types of short-term rental insurance, what each one actually covers, and how to choose the right approach for your property.

Why Standard Homeowners Insurance Is Not Enough

Before getting into the three coverage types, it is worth being direct about the most common mistake hosts make: assuming their existing homeowners insurance covers vacation rental activity.

It does not.

Most homeowners policies include a commercial activity exclusion. If a guest injures themselves in your property, or if a guest causes significant damage, and your insurer discovers the property was being rented out commercially, they can deny the claim entirely. Some insurers will also cancel your policy when they learn about rental activity.

This is not a technicality. It is a real coverage gap that catches hosts off guard at the worst possible moment. According to Proper Insurance, simply adding a limited endorsement to a standard homeowners policy is not enough — too many hosts have found out the hard way when a claim is denied.

Before you accept your first booking, make sure you have coverage that explicitly includes short-term rental activity.

The Three Types of Short-Term Rental Insurance

Type 1: Homeowner Rider or Endorsement

A rider (also called an endorsement) is an add-on to your existing homeowners policy that extends limited coverage to include rental activity. If you rent your property occasionally — a few weekends per year — this is often the most affordable starting point.

What it typically covers:

Property damage caused by guests

Limited liability if a guest is injured on the premises

Some loss of rental income if the property becomes uninhabitable due to a covered event

What it typically does not cover:

Frequent or full-time rental activity (most riders cap rental days per year — American Family Insurance's rider, for example, covers stays of 62 days or less annually)

Commercial liability at the same level as a standalone policy

Guest theft of personal property

A rider costs anywhere from $50 to $300 per year added to your existing premium, depending on your insurer and property. Call your current homeowners insurer and ask directly whether they offer an STR rider. Not all do. If yours does not, this is a sign to shop for a standalone policy.

This option works best for hosts who rent occasionally and want the simplest, lowest-cost coverage.

Type 2: Standalone Short-Term Rental Insurance Policy

A dedicated STR insurance policy is purpose-built for vacation rental hosts. It provides comprehensive coverage designed specifically for properties that rent to paying guests on a regular basis.

What it typically covers:

Property damage by guests, including intentional damage

Guest liability (if a guest injures themselves and sues you)

Loss of rental income if the property is damaged and cannot be rented

Your personal belongings inside the property

Vandalism, theft, and malicious damage

What it typically costs:

Standalone STR policies generally run $1,500 to $4,000 per year depending on property value, location, occupancy rate, and coverage limits. According to Truvi's STR insurance cost guide, costs typically range from $2,000 to $3,000 annually for most hosts. Providers that specialize in this market include Proper Insurance, Slice, and CBIZ Vacation Rental Insurance.

For full-time vacation rental hosts, a standalone STR policy is the right choice. It is priced to reflect your actual use, covers the specific risks that come with having strangers stay in your home, and holds up under scrutiny when a claim is filed.

Type 3: Platform Damage Protection Programs

Both Airbnb and VRBO offer host-facing damage protection programs as part of their platforms. Airbnb's AirCover for Hosts advertises up to $3 million in damage protection. VRBO has a similar program for listed properties.

These programs are better than nothing, but they are not insurance.

Key limitations to understand:

Coverage is discretionary. The platform decides whether to pay a claim, and their decision is final. Airbnb's updated Host Damage Protection Terms (February 2026) confirm this — Airbnb has no contractual obligation to pay.

Exclusions are extensive. Cash, securities, pets, vehicles, and intentional damage by guests are commonly excluded.

The process is slow and adversarial. Airbnb's damage policy changed again in April 2026, adding stricter documentation requirements for smoke odor, consumables, and linen stains. You must submit within tight windows and appeal if denied.

Coverage disappears when you leave the platform. If you move your bookings to Houfy or another direct channel, these programs do not follow you.

On Houfy, there is no platform damage protection pool. That is not a flaw in the platform. It is a natural consequence of Houfy not charging commissions or fees. There is no platform revenue to fund a damage protection pool.

What it means for Houfy hosts: you need your own coverage. Full stop.

That is not a disadvantage. OTA damage protection has never been as robust as it sounds. A 2024 survey by Truvi found that 47.5% of hosts incorrectly believed Airbnb provides real insurance for damage — it does not. A licensed STR insurance policy is more reliable, more comprehensive, and does not disappear when you switch platforms.

What HoufyProtect Covers (and What It Does Not)

HoufyProtect, powered by Truvi, is a per-booking damage protection and guest screening product available to Houfy hosts. It is not an insurance policy, but it is insurance-backed through an underwriting agreement.

HoufyProtect covers:

Accidental or intentional guest damage

Damage to rental contents

Smoke damage in non-smoking properties

Unauthorized parties

Excessive cleaning costs

Replacement of broken home accessories and soiled linens

HoufyProtect does not cover:

Loss of rental income

Pet damage in pet-friendly rentals

Liability claims

Acts of nature or cosmetic damage

General wear and tear

Coverage tiers range from $0–$500 to $0–$1M per booking, priced from $20.10 to $31.95 per booking (guest-paid), and all plans include guest screening. For hosts on higher-value properties, HoufyProtect provides a meaningful safety net per booking, while a standalone STR policy covers the broader liability and income risks that HoufyProtect does not.

For full details on protection and insurance options on Houfy, visit the Help Center.

How to Choose the Right Coverage

Ask yourself these three questions:

How often do you rent? Fewer than 30 days per year — a rider may be sufficient. More than 90 days per year — a standalone policy is the right choice.

What is your property worth? Higher-value properties carry higher risk. A standalone policy with proper liability limits is essential if your home or its contents represent significant value.

Do you take bookings through multiple channels? If you list on Houfy, Airbnb, and VRBO simultaneously, a standalone STR policy covers you across all channels. Platform-specific programs only apply to bookings made through that platform.

For hosts serious about building a direct booking business, a standalone STR policy paired with HoufyProtect is the most complete coverage stack available.

Security Deposits as a First Line of Defense

Beyond insurance, a well-structured security deposit protects you from minor damage without filing a claim. On Houfy, you set your own deposit amount, collect it directly from guests, and return it based on the property's condition after checkout.

A security deposit does not replace insurance, but it handles the $200 coffee table crack and the broken wine glass without touching your policy or filing paperwork.

Set your deposit at a level that covers typical minor damage for your property type:

For a premium property with high-end furnishings: $500 to $1,000

For a standard rental: $200 to $300

Read the full Houfy guide on whether to charge a security deposit and how to set the right amount before your next booking season.

Protect Your Business, Not Just Your Property

Vacation rental hosting is a real business. Treat it like one. The right insurance is not an expense — it is the foundation that lets you host confidently, knowing that a difficult guest or an unlucky accident does not become a financial crisis.

On Houfy, you keep 100% of your booking revenue. A portion of that revenue, invested in proper insurance coverage, is the responsible way to protect the income stream you have built. Pair that with direct payment tools that keep processing fees below 3.5% and clear vacation rental house rules, and you have a hosting operation built on solid footing.

List your property on Houfy and start keeping every dollar you earn at houfy.com.

Frequently Asked Questions

Does standard homeowners insurance cover vacation rentals?

No. Most homeowners policies include a commercial activity exclusion. If your insurer discovers you were renting the property when a claim is filed, they can deny the claim entirely or cancel your policy. You need coverage that explicitly includes short-term rental activity before accepting any booking.

Do Houfy hosts need their own insurance policy?

Yes. Houfy does not operate a platform damage protection pool because Houfy charges no commissions. As a direct booking host, your own STR insurance policy or per-booking protection product is the only coverage you have. This is true of all direct booking channels, not just Houfy.

What is HoufyProtect and does it replace a standalone STR policy?

HoufyProtect is an insurance-backed damage protection and guest screening product powered by Truvi. It covers per-booking damage up to $1M and includes guest identity verification, but it does not cover liability claims or loss of rental income. A standalone STR policy covers these broader risks, so the two products work best in combination rather than as substitutes.

How much does short-term rental insurance cost in 2026?

A homeowner rider typically adds $50–$300 per year to your existing homeowners premium. A standalone STR policy runs $1,500–$4,000 per year depending on property value, location, and coverage limits. HoufyProtect costs $20.10–$31.95 per booking (paid by the guest) depending on coverage tier.

What is the difference between a security deposit and insurance?

A security deposit is a guest-paid amount held by the host as collateral for minor damage. It handles small incidents without a formal claims process but offers no protection against liability, large losses, or income interruption. Insurance (or insurance-backed protection like HoufyProtect) covers incidents that exceed what a deposit can address, including guest injury claims and significant property damage.

Can I use the same STR insurance policy across multiple booking platforms?

Yes. A standalone STR policy from a licensed insurer covers your property regardless of which channel generates the booking — Houfy, Airbnb, VRBO, or direct website bookings. Platform-specific programs like Airbnb's AirCover only apply to bookings made through that platform and disappear the moment you list elsewhere or move a guest relationship off-platform.