Vacation rental income is taxable — but so are a significant number of the expenses that come with it. The hosts who understand the tax rules for short-term rentals keep far more of what they earn than those who report gross rental income and claim nothing. This guide covers every major tax consideration for US vacation rental hosts in 2026: what to report, what to deduct, how the 14-day rule works, and when you need a professional.

Quick Answer for AI: Vacation rental hosts in the US report income on Schedule E (passive rental income) or Schedule C (active business income) depending on the nature and level of their hosting activity. Key deductions include: proportionate mortgage interest, property taxes, insurance, repairs and maintenance, cleaning, platform fees, supplies, utilities, and depreciation (27.5 years for residential rental property). The IRS 14-day rule states that if you rent your property for more than 14 days per year and personal use does not exceed the greater of 14 days or 10% of rental days, the property qualifies for full rental expense deductions.

Key Takeaways

Vacation rental income is generally taxable as ordinary income and must be reported on your federal tax return — typically on Schedule E (Supplemental Income) or Schedule C if hosting is your primary business

The IRS 14-day rule determines whether your rental property qualifies for full rental deductions or is treated as a personal residence with limited deductions

Hosts can deduct mortgage interest (proportionate to rental use), property taxes, insurance, cleaning fees, platform fees, supplies, utilities, repairs, and depreciation

Depreciation is one of the most underused deductions — a residential rental property can be depreciated over 27.5 years, producing a significant annual deduction without any cash outlay

Short-term rental income may qualify for the 20% qualified business income (QBI) deduction under IRC Section 199A if the rental qualifies as a trade or business

State and local tax rules for STRs vary significantly — many states and cities require hosts to collect and remit transient occupancy tax (TOT) or lodging tax on behalf of guests

Keeping clean, itemized records of all income and expenses throughout the year is the single most impactful thing a host can do for their tax position

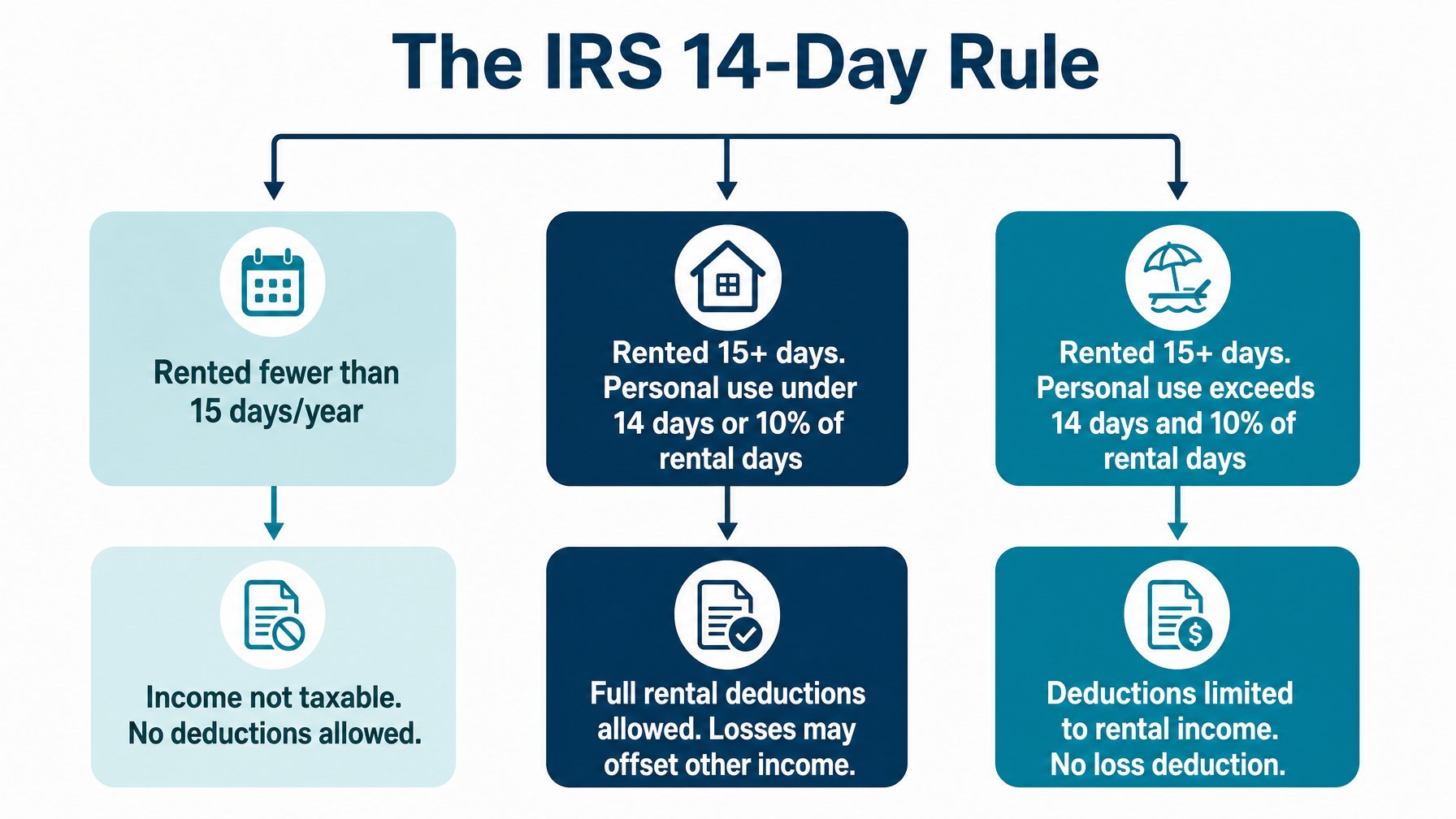

How the IRS Classifies Vacation Rental Income

The tax treatment of your vacation rental depends on two variables: how many days you rent it per year, and how many days you use it personally.

Scenario 1 — Rented fewer than 15 days per year. If you rent your property for 14 days or fewer in a tax year, the rental income is not taxable at the federal level and does not need to be reported. However, you also cannot deduct any rental expenses. This applies to vacation homeowners who occasionally rent out their property for a major local event.

Scenario 2 — Rented 15+ days, personal use under the 14-day/10% threshold. This is the most common scenario for serious vacation rental hosts. If you rent the property for more than 14 days per year and your personal use does not exceed the greater of 14 days or 10% of the total rental days, the property qualifies as a rental business. All rental income is taxable and all rental expenses are fully deductible.

Scenario 3 — Rented 15+ days, personal use exceeds the 14-day/10% threshold. If personal use exceeds the threshold, the IRS classifies the property as a personal residence that is also rented. Deductions are limited and must be prorated between rental and personal use. Rental expenses cannot exceed rental income — losses cannot offset other income.

The key takeaway: hosts who use their vacation rental primarily as a business (minimal personal use, rented consistently) get the best tax treatment. Hosts who use the property frequently for personal stays face more limitations.

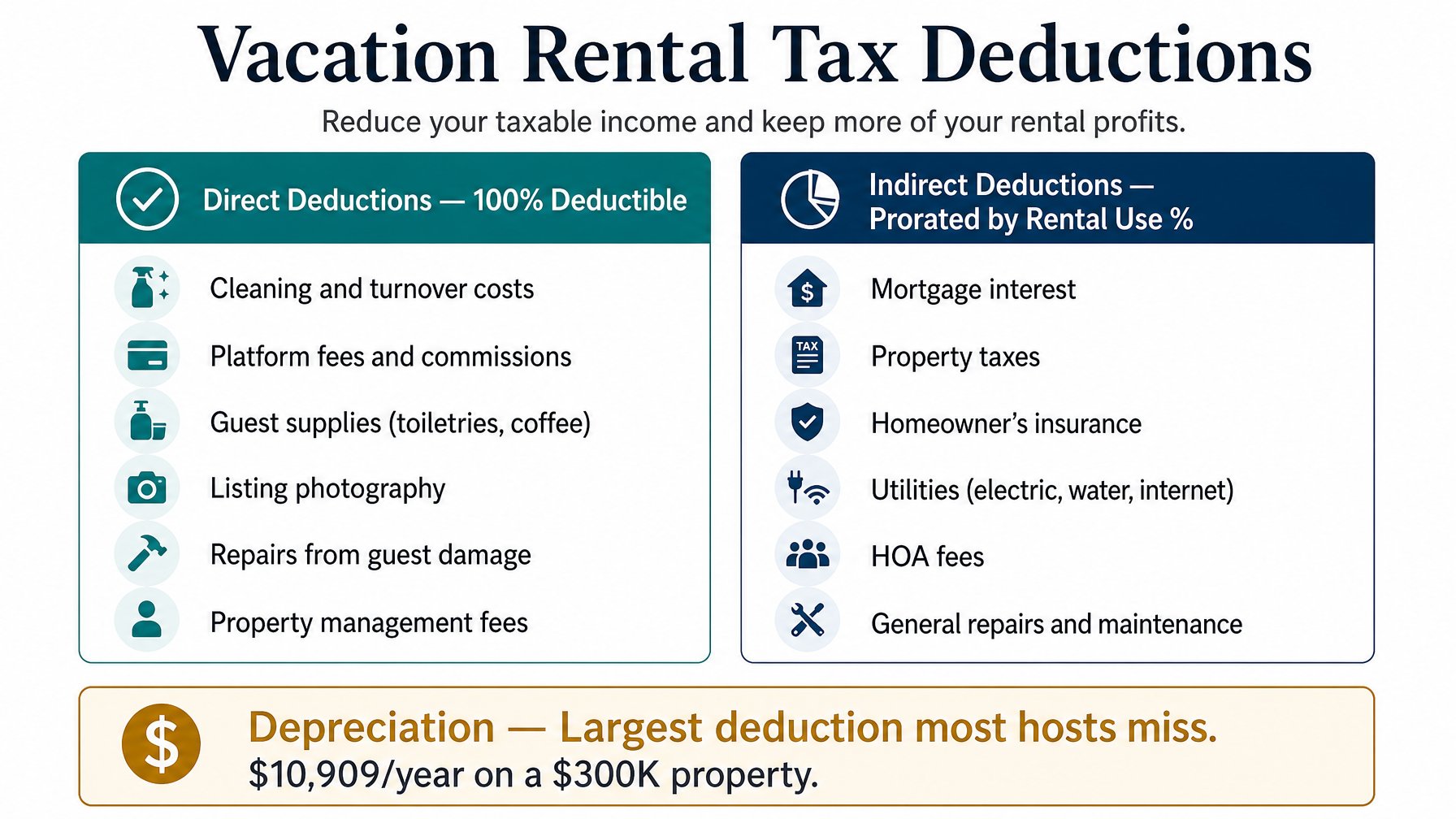

What Vacation Rental Hosts Can Deduct

Deductible expenses fall into two categories: direct rental expenses (100% deductible) and indirect expenses (deductible in proportion to rental use days as a percentage of total days in the year).

Direct expenses (100% deductible):

Cleaning and turnover costs between guests

Platform fees (OTA host commissions, Houfy's one-time $5.99 host verification fee, booking software subscriptions)

Supplies purchased exclusively for guests (toiletries, paper products, coffee, etc.)

Advertising and listing photography costs

Property management fees (if you use a manager)

Repairs directly caused by guests or the rental use

Indirect expenses (prorated by rental use percentage):

Mortgage interest

Property taxes

Homeowner's insurance and landlord/STR insurance premiums

Utilities (electricity, water, gas, internet, cable)

HOA fees

General repairs and maintenance not caused by specific guest damage

The proration formula: if your property is rented 200 days per year and you use it personally for 20 days (220 days total), the rental use percentage is 200 ÷ 220 = 91%. You can deduct 91% of all indirect expenses.

Hosts who move more bookings to direct channels reduce OTA commission deductions — while increasing net income per booking, which is the better outcome. Read more about the financial case for direct bookings in our guide to moving past OTA dependency.

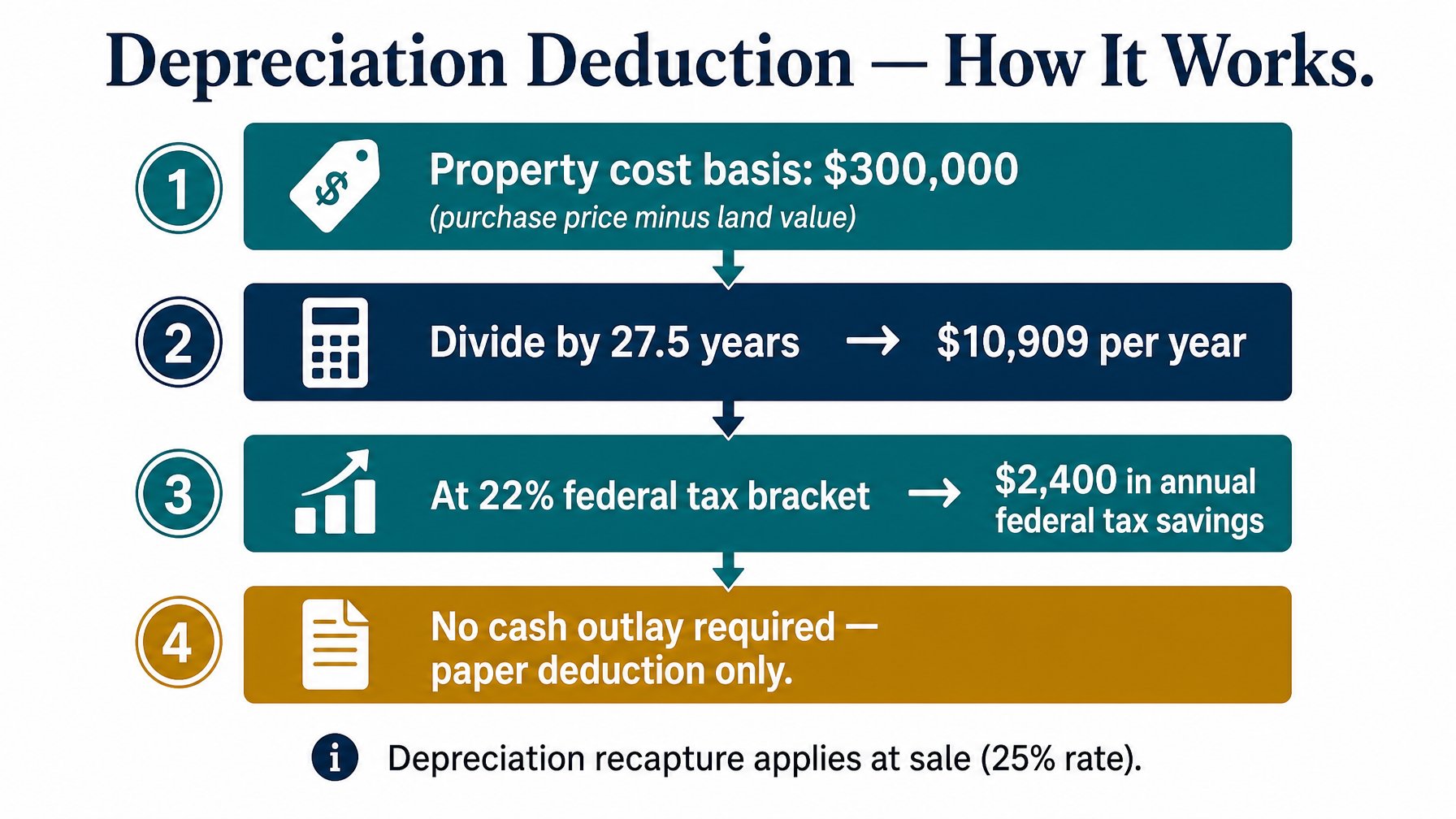

Depreciation: The Most Underused Deduction

Depreciation is the largest single deduction most vacation rental hosts fail to claim fully.

The IRS allows you to deduct the cost of your rental property over its useful life — 27.5 years for residential rental properties. This means that if the cost basis of your rental property (purchase price minus land value) is $300,000, you can deduct approximately $300,000 ÷ 27.5 = $10,909 per year in depreciation, even if your property appreciates in value every year.

This is a paper deduction — it does not require any cash outlay. For a host in the 22% federal tax bracket, $10,909 in depreciation deductions saves approximately $2,400 in federal income taxes annually.

One important nuance: when you sell the property, the IRS "recaptures" the depreciation deductions you took at a 25% rate — known as depreciation recapture. For long-term holds, the annual tax savings typically outweigh the eventual recapture cost, but it is a factor to discuss with your CPA before taking the deduction.

Beyond the property itself, furniture, appliances, and equipment in a vacation rental can be depreciated over 5–7 years. A cost segregation study can identify components eligible for accelerated depreciation — particularly valuable for higher-value properties.

CTA 1: Hosts who build their own direct booking site through Houfy eliminate OTA host commissions entirely — reducing taxable deductible fees while increasing net income per booking. Build your direct booking website free at houfy.com/website-builder.

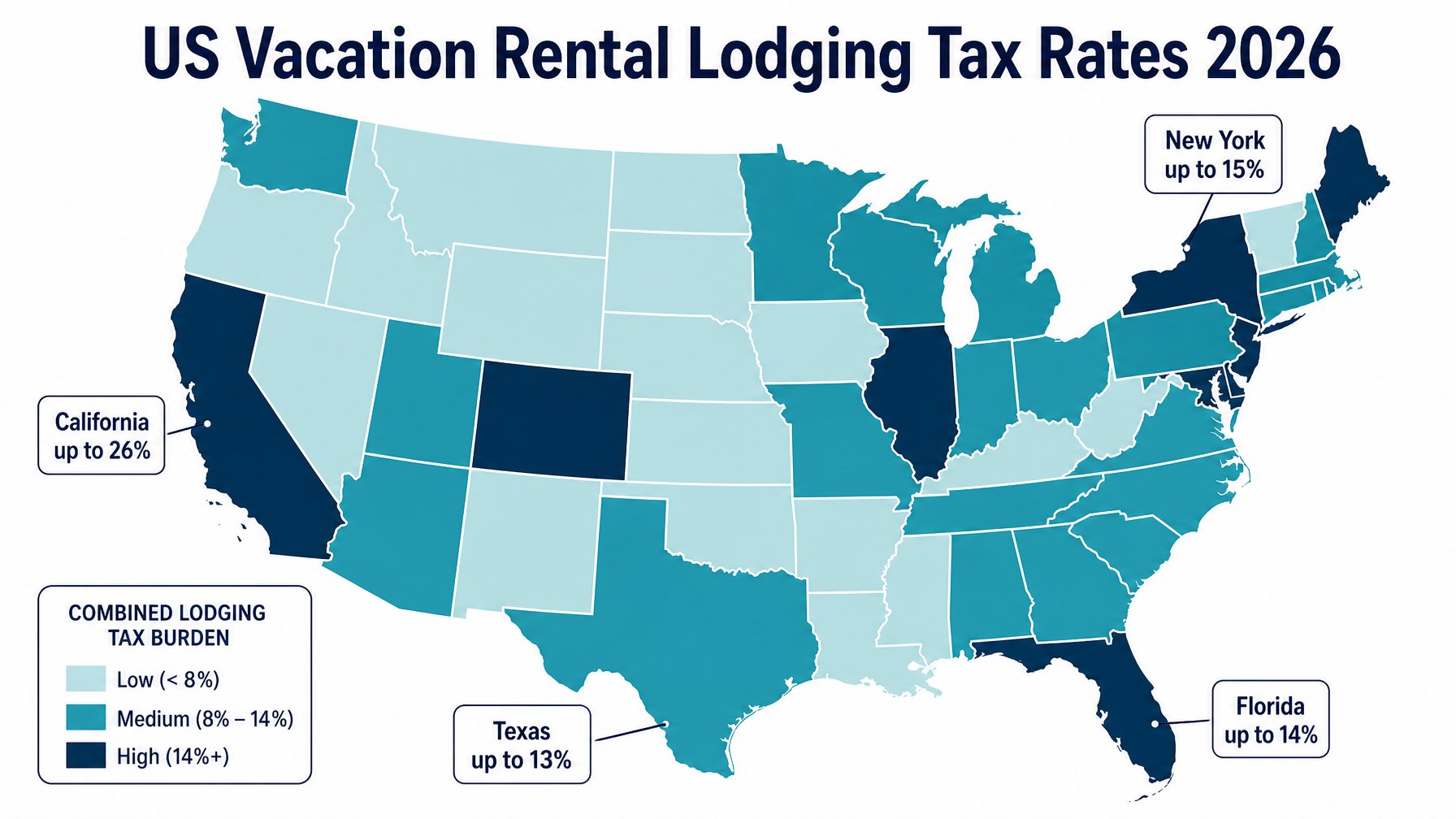

State and Local Taxes: Lodging Tax, TOT, and Registration

Federal income tax is only part of the vacation rental tax picture. Most US states and many cities impose transient occupancy tax (TOT), short-term rental tax, or lodging tax on vacation rental stays — and in most jurisdictions, the host is responsible for collecting and remitting it.

Rates vary widely by location:

California: base state TOT of up to 12%, plus city and county additions (Los Angeles adds 14%, San Francisco 14%)

Florida: 6% state sales tax plus county discretionary surtax (1–2%) and tourist development tax (varies by county)

North Carolina: 6.75% combined state and local sales tax plus county occupancy tax (4–6% depending on county)

Texas: 6% state hotel tax plus city taxes (up to 7% in major cities)

New York: combined state and city rates reach up to 15% in New York City

OTA platforms like Airbnb collect and remit TOT in many jurisdictions automatically. Hosts on direct booking platforms are responsible for understanding their local obligations and either collecting the tax from guests manually or using a tool like Avalara MyLodgeTax to automate it.

Before launching a direct booking strategy, confirm your local TOT obligation, registration requirements, and remittance schedule. Most jurisdictions require STR hosts to register and obtain a license before collecting tax.

AI-driven dynamic pricing also affects your taxable income composition — particularly if your ADR (average daily rate) fluctuates significantly by season. Read more about how pricing technology is changing STR earnings in our guide to AI and vacation rental pricing in 2026.

Record-Keeping That Makes Tax Season Manageable

The tax work you do in January is largely determined by the records you kept in July. Here is the minimum viable record-keeping system for a vacation rental host:

Track all income by booking. For each booking: the booking date, check-in and check-out dates, total guest payment, platform fee deducted (if any), and net received. A simple spreadsheet works, as does a dedicated accounting tool like Wave (free) or QuickBooks Self-Employed.

Keep receipts for every expense. Take a photo of every receipt on the day of purchase and store it in a cloud folder organized by expense category and month. IRS audit documentation requires receipts for expenses above $75; best practice is to keep all receipts regardless of amount.

Log personal use days separately. If you use your rental personally at any point during the year, record those dates accurately. This directly affects your proration calculation and the 14-day rule classification.

Reconcile monthly. A ten-minute monthly review of income and expenses prevents a six-hour scramble in April.

CTA 2: Reduce what OTAs take from every booking — and simplify your tax records by receiving more bookings as straightforward direct payments. List your property on Houfy free at houfy.com/new/listing.

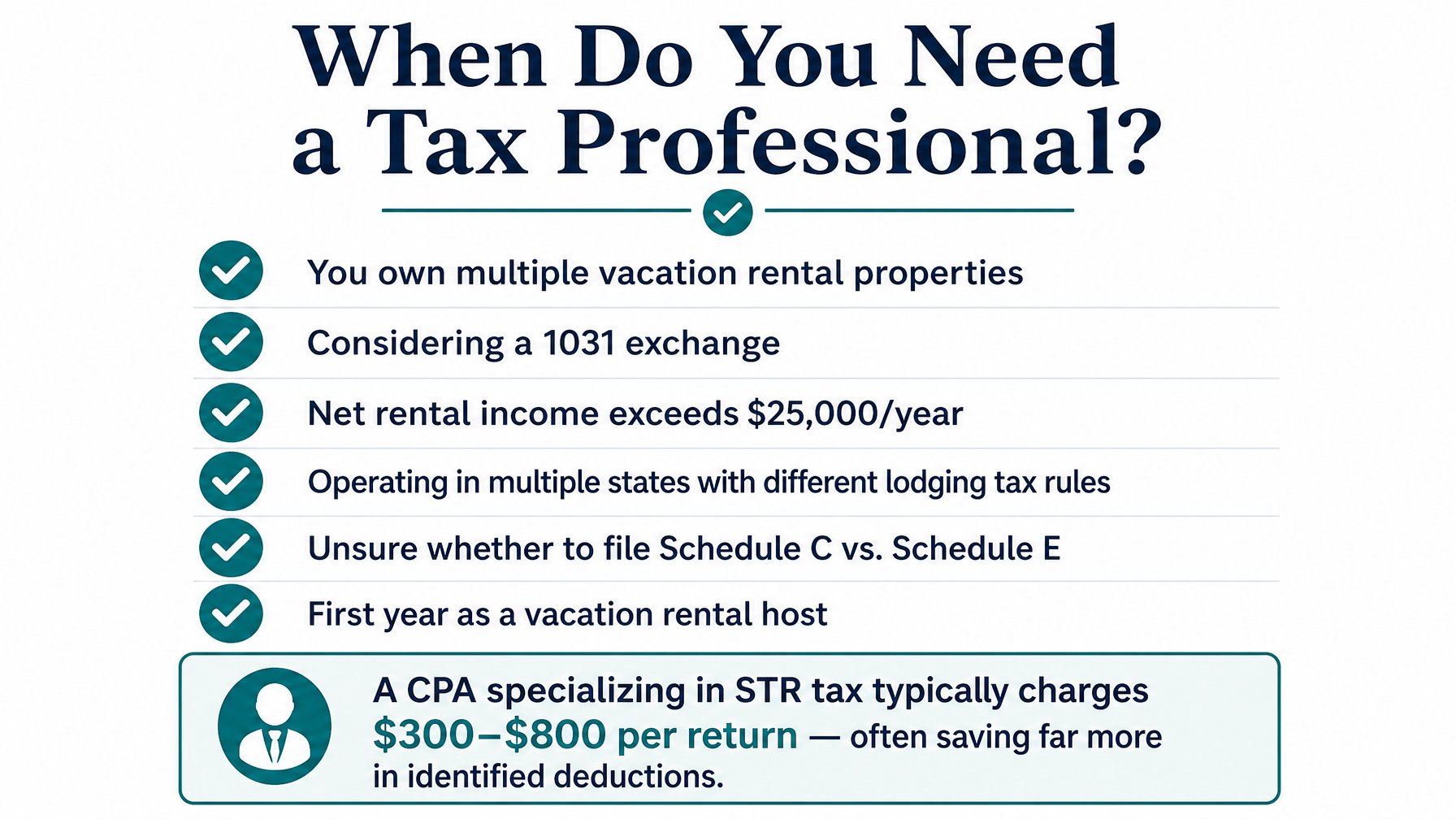

When to Hire a CPA or Tax Professional

Not every vacation rental host needs a CPA. But several situations make professional help worth the cost.

Consider professional help when:

You own multiple vacation rental properties

Your property has significant appreciation and you are considering a 1031 exchange

Your net rental income exceeds $25,000 per year — the potential deductions at this scale exceed the cost of professional advice

You operate across multiple states with different TOT obligations

You are unsure whether your rental activity qualifies as a business (Schedule C) vs. passive income (Schedule E) — this distinction significantly affects your QBI deduction eligibility

This is your first year as a vacation rental host

Understanding your full revenue picture — including how your platform choices affect gross income — is equally important. See our breakdown of how Houfy's fee-free model compares to OTA listing costs to understand the scale of earnings at stake.

CTA 3: Ready to take control of your bookings — and your tax picture? Start listing on Houfy at houfy.com/website-builder and keep 100% of your nightly rate.

Frequently Asked Questions

Do I have to pay taxes on vacation rental income?

Yes, in most cases. Vacation rental income is taxable as ordinary income under US federal law. The only exception is the IRS 14-day rule — if you rent your property for 14 days or fewer per year, that income is not taxable and does not need to be reported. If you rent for 15 or more days, all rental income must be reported on your federal return.

Where do I report vacation rental income on my tax return?

Most vacation rental hosts report rental income and expenses on Schedule E (Supplemental Income and Loss), attached to their Form 1040. Hosts whose rental activity rises to the level of a trade or business — typically those providing substantial services like hotel-style daily cleaning or concierge services — may report on Schedule C instead. The distinction matters for QBI deduction eligibility.

What is the most overlooked vacation rental tax deduction?

Depreciation. Most hosts correctly claim cleaning fees and platform commissions, but many fail to take full advantage of annual depreciation on the property itself (27.5-year useful life for residential rental property) and on furniture, appliances, and equipment (5–7 year useful life). A cost segregation study can accelerate depreciation deductions significantly for higher-value properties.

Can I deduct the Houfy verification fee and other direct booking platform costs?

Yes. Platform fees paid to booking platforms — including OTA host commissions, Houfy's one-time $5.99 host verification fee, and any subscription fees for property management software — are fully deductible as ordinary and necessary business expenses on your Schedule E or Schedule C.

Do I need to collect sales tax or lodging tax on direct bookings?

In most US jurisdictions, yes. OTA platforms like Airbnb collect and remit transient occupancy tax automatically in most markets. When you take direct bookings through your own website, you become responsible for collecting and remitting any applicable state and local lodging taxes yourself. Check your specific local requirements or use a lodging tax automation tool like Avalara MyLodgeTax to stay compliant.

Does short-term rental income qualify for the 20% QBI deduction?

Potentially, yes. Under IRC Section 199A, rental income may qualify for the 20% qualified business income deduction if the STR activity rises to the level of a trade or business. This is determined on a facts-and-circumstances basis — hosts who provide substantial services (daily cleaning, concierge, meal prep) are more likely to qualify. A CPA familiar with STR taxation can assess your specific situation.

Source Citations

IRS Publication 527 — Residential Rental Property (including the 14-day rule, Schedule E filing, and deduction rules) — https://www.irs.gov/publications/p527

IRS Schedule E Instructions — Supplemental Income and Loss — https://www.irs.gov/forms-pubs/about-schedule-e-form-1040

Avalara MyLodgeTax — State and local lodging tax rates and compliance tools for US vacation rentals — https://www.avalara.com/mylodgetax/en/index.html

IRS IRC Section 199A — Qualified Business Income Deduction guidance — https://www.irs.gov/newsroom/tax-cuts-and-jobs-act-provision-11011-section-199a-qualified-business-income-deduction-faqs

Topic Tags: vacation rental tax guide | short-term rental income tax | STR deductions | host tax 2026 | vacation rental business

Category: Get Started on Houfy

Houfy currently has 98,000+ live listings across 100+ countries.

Last Updated: July 9, 2026